How to Buy Car Insurance

What Kind of Car Insurance Should I Buy in Georgia?

When families call me for advice after their crash, we start by exploring the insurance coverages the family has. I often hear “well, we have full coverage.” That means very little. Full coverage, in the parlance of insurance agents, means that you have collision, comprehensive, liability and uninsured motorist coverage. It does not mean you have good coverage.

In order to make you a smarter consumer, I will first explain what types of coverage there are and then we will discuss how to make sure you have the best.

STEP 1: Understand the Types of Insurance Available on an Auto Policy

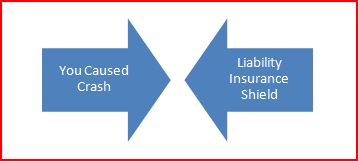

There are various types of coverage in a car insurance policy, and it helps to think of each one as a unique shield that protects against different hazards. The arrows below illustrate the threat that each type of coverage protects you against. Liability Insurance Coverage

“Liability/Bodily Injury” Coverage

This is one of the most important coverages. If you collide with someone or something and a person is injured or property is damaged, this coverage steps up to protect you. Let us discuss a specific example. If you hit Steve and Betty Smith and they get hurt and have medical expenses, your insurance company will do two things for you if a claim is made. 1) Your insurer will pay the Smiths up to your coverage limits, if the insurer determines the claim is worth that much. (indemnity) 2. The Insurer will provide you with a free lawyer if you get sued. (“the duty to defend”)

Let us assume that you have $50,000.00/$100,000.00 in coverage. (the first number is the per person limit, the second is the per-incident maximum)You hit the Smiths and the collision breaks their legs. Under a policy that lists $50,000/$100,000.00, the policy would pay up to $50,000.00 to each of them, if appropriate. If they had smaller injuries, the dollar amounts would be more appropriate to the injury. If there were five people injured, your policy would pay out a maximum of $100,000.00 total.

Liability Coverage for Property Damage

This coverage gives you indemnity for damage you cause to other property. It pays for your mistake if you hit your neighbor’s fence or run into their car. Your insurance company will investigate and appraise the damage and pay the appropriate amount for the damage you caused up to your policy limits.

To recap, Liability coverage protects you from other people that come after you when you harm a person or property on accident. I suggest that you carry a minimum of $100,000.00/$300,000.00 in liability insurance. Please note that there is no coverage for you if you cause harm or damage on purpose as the consequences of intentional acts are not insured against.

Uninsured/Underinsured Motorist Coverage

Uninsured/Underinsured Motorist Coverage is the most important coverage. Match your amount of liability coverage to the Uninsured Motorist Coverage !!! Why?

Uninsured Motorist Insurance was authorized by a Georgia law, O.C.G.A. 33-7-11 . O.C.G.A. stands for Official Code of Georgia Annotated. If you see that phrasing it is telling you that the relevant law can be found in the Georgia code title 33, chapter 7, section 11. I cannot emphasize enough how important it is to have Uninsured and Underinsured Motorist coverage at the same levels as your liability coverage.

What kind of drivers do you think cause the most devastating injuries in car accidents? You guessed it; they tend to be caused by uninsured and underinsured drivers. Bad drivers tend to have a lot of speeding tickets and prior collisions and cannot afford decent insurance coverage. As a result, careless drivers usually have crummy insurance and do not have enough liability insurance to pay for serious medical bills. When that happens, the only thing protecting you is your uninsured/underinsured motorist coverage. You must protect yourself against these people.

Georgia only requires that people have $25,000.00 in liability insurance, this is the minimum mandatory amount. That may seem like a lot of money, but that’s only if you have not been to the hospital recently. For example, in Metro Atlanta, the typical ambulance ride costs $600.00, the Emergency room visit is at least $800, X-Rays cost around $250.00, an MRI is $1100, a CT scan can cost $2,000.00 and so on. Even a modest trip to the emergency room usually costs around $2,000.00. Then there can be mountains of bills from physical therapy and medications. In short, even a simple auto accident case with sprained muscles that requires an Emergency room visit and physical therapy can leave a person with over $5,000.00 in bills. If there are any broken bones, the medical bills alone can quickly exceed $25,000.00, not to mention the lost wages.

As of January 1, 2009, there are now two kinds of Uninsured Motorist Insurance that you can buy.

Added-On Uninsured/Underinsured Coverage

This is the best type and only costs around $50.00 more than regular uninsured motorist coverage. If you own this type of coverage it sits on top of any insurance that the careless driver has. How does added-on uninsured coverage work?

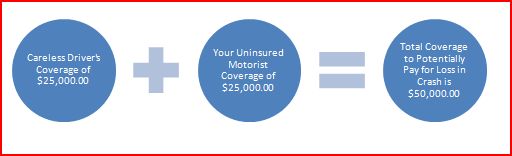

Take for example my client “Jane.” Jane had a compound fracture of both lower leg bones when a 22-year-old driver pulled out in front of her in North Georgia. Over the next year, she underwent two surgeries and months of painful physical therapy. She also lost her job. Her case had a value in excess of $300,000.00. The other driver only had $25,000.00 in insurance coverage (the minimum in Georgia). If Jane did not have uninsured motorist coverage, then it would not matter how bad the injury was. A young driver with no assets is essentially judgment proof and there would be nothing more than the $25,000.00 policy available to Jane, which would not even cover the medical bills. Thankfully she had three Added On type $250,000.00 uninsured motorist policies that I was able to stack on top of each other so there was $775,000.00 in available coverage. Jane protected herself from the carelessness of others by buying good insurance.

Non-Stacking Uninsured/Underinsured Insurance Coverage

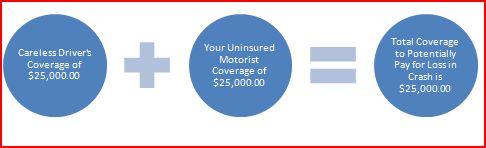

This coverage is a distant second to added-on type coverage. It will not stack on top of the at-fault driver’s coverage. For example, if you are hit by a driver with $25,000.00 in coverage and you have $25,000.00 of this type of coverage, then your insurance company is in the shadow of the careless driver’s coverage and $25,000.00 is the maximum amount of insurance money available to you. (Your policy minus at-fault policy yields coverage available)

To recap; if you buy added-on coverage it works like this:

Non-stacking Coverage would look like this:

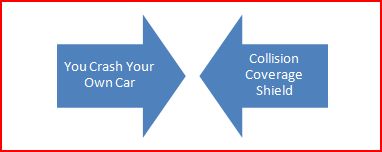

Collision Coverage

Collision coverage protects you against yourself when you cause a crash either with another vehicle or with an object. It will pay to repair damage you or a “permissive user” causes to your own vehicle. A “permissive user” is someone that you allow to drive your car. It is required on cars that you finance or lease. You have a good deal of control over the rates as you can set a deductible. The idea is that if you crash your car and the repairs cost $5,000.00 then you pay the deductible and the company pays the rest.

Comprehensive Loss Coverage

Comprehensive insurance is a catch-all coverage that protects you against a variety of dangers. If you have it, you are insured if the car is stolen, struck by lightning, flooded out, struck by hail, or hit by a tree. If your car is more than 10 years old or not worth much, I would not worry about getting it.

Medical Payments Coverage (Med Pay)

If your agent cares about you or you are tuned in, you will put medical payments insurance on your Georgia car insurance policy. This coverage directly benefits you and your passengers in the event that you are hurt in an accident. It pays regardless of who caused the accident and does not have to be repaid if you make a recovery later against an at fault party unless you get “made whole” by an eventual settlement. This coverage is comparatively inexpensive, and I highly recommend that you at least get $5,000.00 in coverage.

Step 2: Determine What Coverage You Have

Now that we know what the different coverages are, you need to figure out what you have. You can look at the last renewal mailing the company sent, pull it up online or call your insurer and ask. If you pull it up online or look at the renewal paperwork, you will see a declarations page. The declarations page “declares” what coverages you have.

I have “full coverage” and I carry $300,000.00/500,000.00 in limits. That means that if I crash and hurt someone, there is $300,000.00 in insurance available to each person and up to $500,000 available total for injuries in the crash no matter how many people are in the crash. I carry the same amount of Uninsured/Underinsured Motorist Coverage. That means that if I am hurt badly by a driver with small coverages or no coverage, my $300,000 steps up to “act” as though it were that driver’s insurance. I am insured against being hit by a driver with bad insurance.

Step 3: Get a Quote on Increasing Your Insurance Limits to $100,000.00 in Liability AND Uninsured/Underinsured Motorist Coverages from Your Own Company

If you learn nothing else from this book, carry at least $100,000.00 in Liability and UNINSURED/UNDERINSURED MOTORIST COVERAGE!!! Also, carry at least $5,000.00 in medical payments insurance to protect you from your health insurance premium deductible. These numbers are endorsed by the Insurance Institute and Edmonds.com. If your net worth, including home equity, is over $300,000.00, you should also carry an umbrella insurance policy that goes above and beyond the car insurance policy and will also indemnify you for many other types of civil liability.

Step 4: Compare Your Insurance Company’s Quote with Quotes from other Companies and Compare Customer Satisfaction Online

Remember that you can switch car insurance companies at any time or you can wait until the end of the policy period. Although some companies have a small penalty if you cancel early in the policy period, most don’t. Be sure to call and ask. That means you do not have to wait until the end of the policy period to cancel. The company will prorate the premium and send you back any unused premium. You are the consumer; insist on the best companies. I will not write here which companies rate the best for customer satisfaction as it changes frequently. The website for J.D. Powers and Associates lists the best and worst car insurance companies.

If you want to change insurance companies, call your insurer and tell them that you want to cancel your policy and give them an effective date. They will mail you a cancellation request form which you should read carefully and then fill out and return. Make sure that there is no lapse (gap in time) between the old policy and the new policy. Make sure that another insurer has agreed to insure you before you tell your old company you are canceling them.

Incidentally, you can switch insurance companies after a crash. It will not affect what the insurance company decides to do and won’t hurt the coverage that was in place on the day the crash occurred.

Gap Coverage: A Final Warning

One other important thing: if you buy a car, make sure you have gap coverage in place because in the first three years after purchase it is likely that you are “upside-down” (owe more than the car is worth) on your car loan. The at-fault driver does not owe you the amount owed on your loan; they only owe the fair market value of your car at the time that it was destroyed. In other words, if your car gets hit and totaled out and you owe more than it is worth, that is your problem!

Who is Covered by What Insurance When I Borrow a Car or Loan One Out?

When you buy car insurance on your car, you have the right to lend the car out every now and then. When you lend the car to someone, they are a “permissive user” and they are covered by the same coverages you bought for your car. In Georgia, liability coverage “follows the car” which means that if your buddy Larry crashes your car into someone else, your insurance policy steps up first to protect Larry for his mistake, followed by any insurance Larry himself has. Your collision coverage also applies and will pay for the damage to your car, if you have it. Larry is also protected by your uninsured motorist coverage while he is driving or riding in your car, but that coverage comes second to any of his own coverages. So remember if Larry is a crummy driver and he makes a mistake, it is your insurance policy that will pay out first, not his.